👋 Introducing Amplify AI: Fast brand signals for social video

LEARN MOREHot cocoa, snowmen, and more! Holiday innovation that sleighs this year

The holidays are here! No matter what holiday you celebrate, there’s no arguing that this time of year is critical for brands to get right. And for the CPG category, that means turning to seasonal limited editions and new product introductions to drive incremental sales.

But not all limited-time products are created equal. So what makes a good one?

We researched 17 holiday products (from sweet baked snacks, cereal, chocolate and non-chocolate candy categories) selling in the US in 2023 with our advanced concept testing solution, Activate It, to understand their potential based on consumer feedback. Read on to discover what we learned about what makes a successful holiday innovation.

The ultimate guide to successful seasonal innovation

Find out which elements make for a successful seasonal innovation and which you should watch out for based on consumer research.

Less is more! As we expected (we saw the same thing at Halloween this year), keeping the base of a core selling product and making seasonally-relevant enhancements is favorable over pushing a new flavor or brand new product into the market.

And yet specific for holiday products, some new flavor products came out on top as they capitalized on the most popular taste profiles of the season in a way that fit well with the brand. Findings are outlined in more detail below.

But first, a brief explanation of our methodology to help put our findings in context. Activate It is part of our end-to-end innovation suite and provides fast and actionable insights for mid to late-stage innovation.

The system focuses on two key metrics to determine success: Trial Potential and Breakthrough Potential. While Trial Potential is based on the product’s purchase likelihood, Breakthrough Potential is defined by how different and superior the product is perceived to be vs. what’s already available in the market.

The combination of those scores places products within a classification grid to forecast their performance in market and advise on the best launch strategy.

We focused our findings on those two key potential metrics and dive into the detail behind the scores.

Innovation research metrics: Trial & Breakthrough Potential

Learn more about why trial and breakthrough potential is so important and what role they play in innovation development.

To help us understand whether there’s consistency in seasonal innovation performance trends, we segmented the products into the same categories as we did for our Halloween innovation analysis:

Enhanced core products: Everyday products with a Christmas twist — themed-packaging, seasonal shapes, etc.

New* flavors: Products derived from an existing core range with a new flavor launched specifically for the holidays.

New* products: Products launched specifically for the holidays, not stemming from an existing range that is available all year round.

* not necessarily launched this year

Christmas products performed, overall, significantly better than Halloween products across key metrics.

Over half of the products tested showed high Trial and Breakthrough Potential, sitting within the “short term trial” and “scale and sustain” areas of the classification grid. All ‘enhanced core products’ tested landed within the top third of all food products on Trial Potential. And while ‘new flavor’ products didn’t fare well among the Halloween set, some were top performers this time around.

Jingle all the way: Products with highest in-market potential

Before we dive into the ‘new flavor’ products that did well, let’s revisit the winning formula for ‘enhanced core products.’

The winning enhanced core products

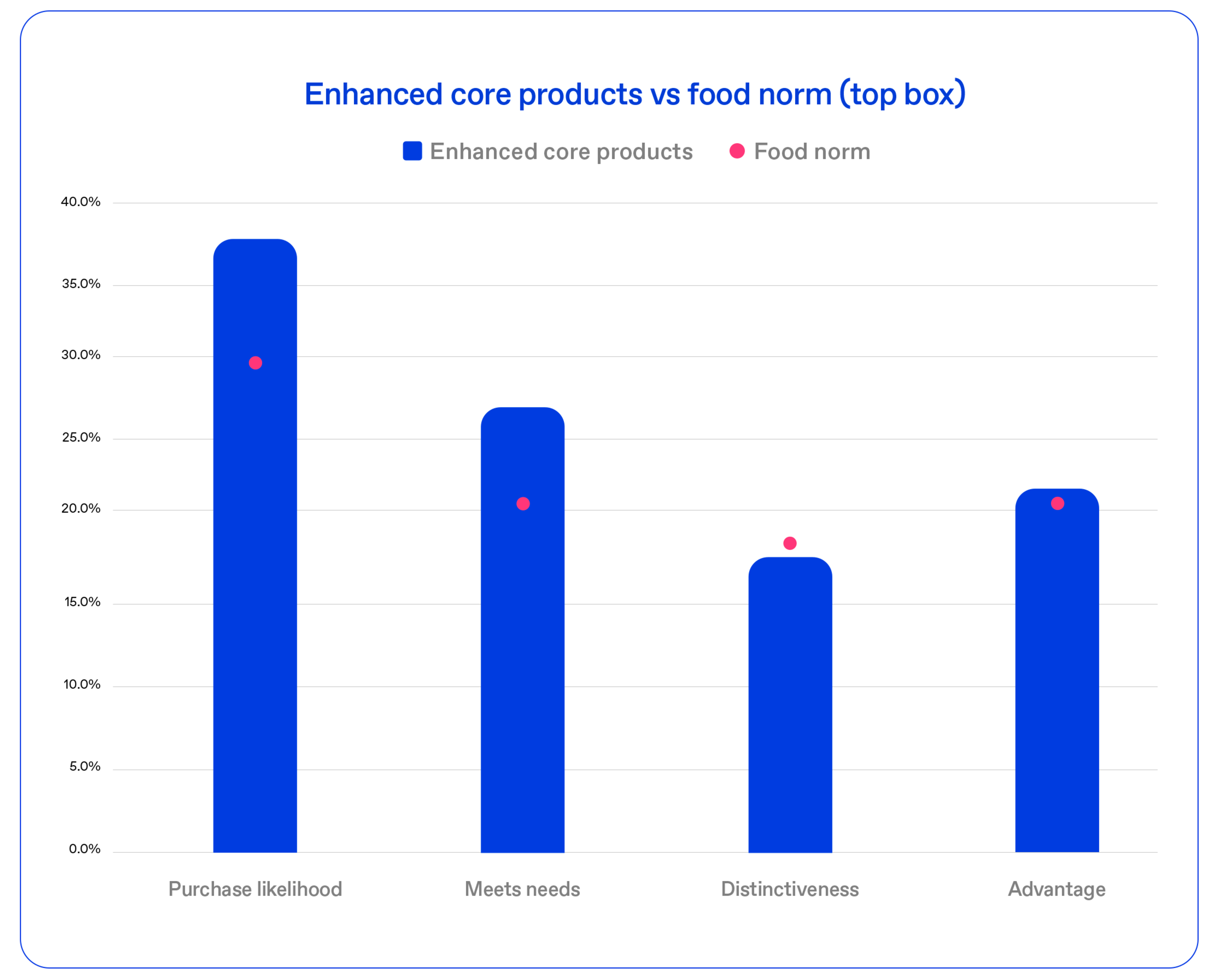

These products may not be hugely differentiated (17.5% top box vs. 18.2% food norm) or superior vs. what’s already in market (21.5% top box vs. 20.3% food norm); but they are significantly more likely to meet consumers’ needs (27.4% top box vs. 20.7% food norm) and drive purchase intent (37.7% top box vs 29.5% food norm) than the average innovation.

After all, they are just products consumers know and love — dressed in festive attire!

Seemingly simple changes to a product’s look and feel can be highly effective and rewarding during seasonal periods. On average, 62% of consumers said they would buy these ‘enhanced core products’ in addition to what they typically buy from their respective categories.

A quick look into some of these successful enhanced core products:

Consumers loved the choice of seasonal colors (red and green) from M&M’s and festive additions to their classic characters and pack designs.

Lindt and Kinder were praised for their extremely adorable figures and for encouraging people to use their chocolates as more than food.

Hershey’s Santa hats were seen as very clever and cute — what a great way to utilize the original shape of the product and make it seasonally relevant!

Reese’s was commended on their seasonal delivery in general (even beyond Christmas). Consumers thoroughly enjoy their different seasonal shapes and are convinced they contain more peanut butter filling than the traditional cup!

The winning new flavors

Beyond the ‘enhanced core products,’ two ‘new flavor’ products performed extremely well — landing in the “scale and sustain” area of the concept classification grid. Both products were from Hershey’s Kisses: a Hot Cocoa and a Candy Cane variant. And given Hershey’s iconic association with the holidays through its long-running festive ad, we aren’t surprised.

Hershey’s Kisses Hot Cocoa scored within the top 3% of food products in the US on both Trial and Breakthrough Potential — proving it to be a Kisses flavor that could perhaps be considered for longer than just the holiday season.

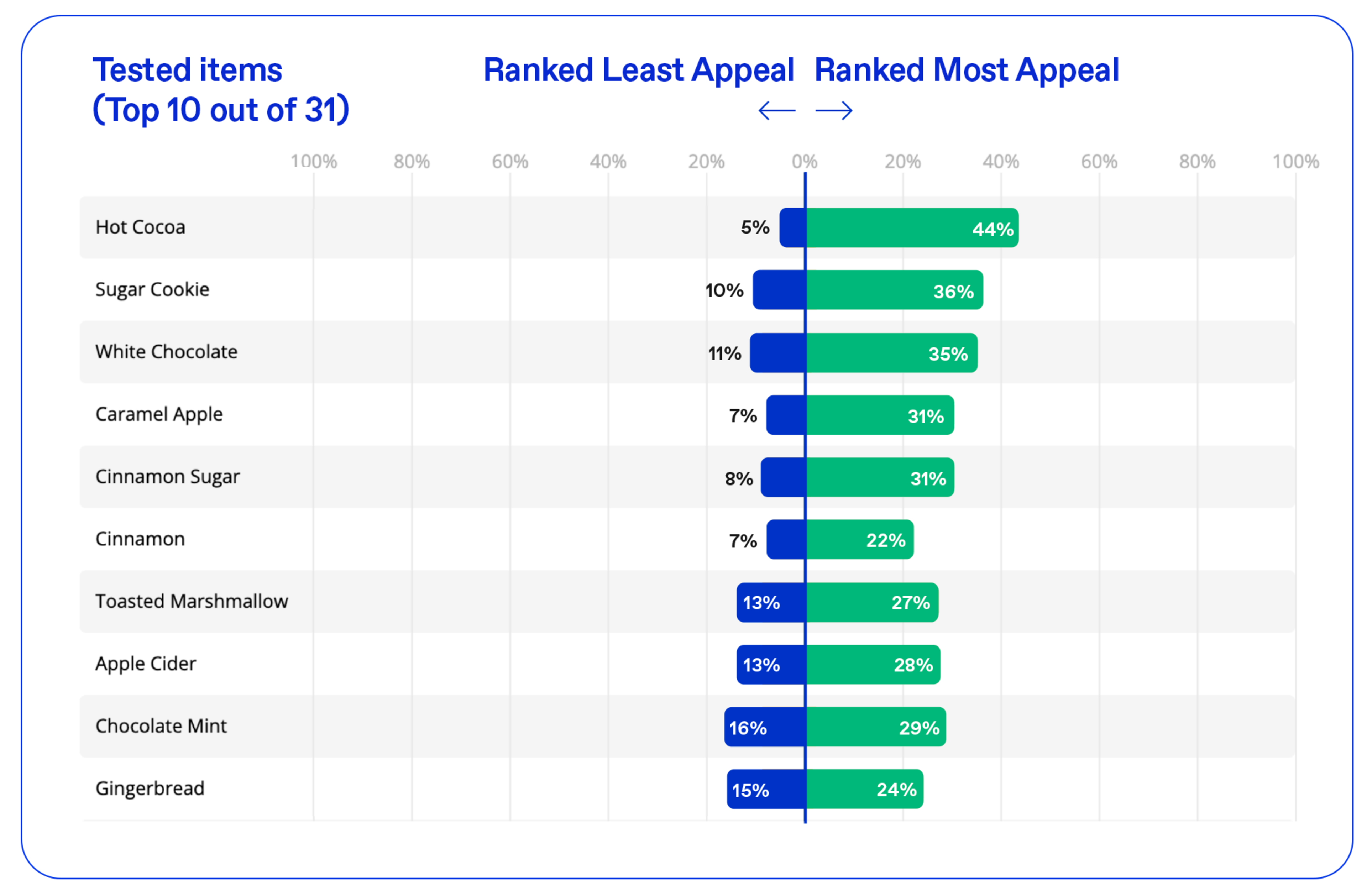

Picking the right flavor for a seasonal innovation is key. Earlier this season we asked US consumers — through our robust MaxDiff screening tool — which seasonal flavors are most appealing to them during the winter holidays. Hot cocoa came out on top, ranked the most appealing flavor most consistently by respondents. Toasted marshmallow also featured in the top 10, which helps explain the success of the Hershey’s kisses Hot Cocoa product. Almost half of respondents mentioned the product’s flavor/ingredients when talking about what they liked about it. Some of the comments about why people loved it included:

“I love Hershey’s Kisses, and these sound really great, especially for the holiday season. Hot chocolate made with milk chocolate and filled with marshmallow cream sounds amazing and like everyone in my family would love them."

"I like that they have a marshmallow filling and I love hot cocoa. This is perfect for the winter and upcoming holiday season.”

Hershey’s also capitalized on the white chocolate trend for holiday products and topped it up with candy cane pieces for the ultimate seasonal combo. About half of consumers said Hershey’s Kisses Candy Cane would make them want to buy from the brand more frequently. One of our respondents said: “I like that this is a nice holiday treat with a delicious candy cane twist. This is great for entertaining and filling a candy dish. It's also a great stocking stuffer."

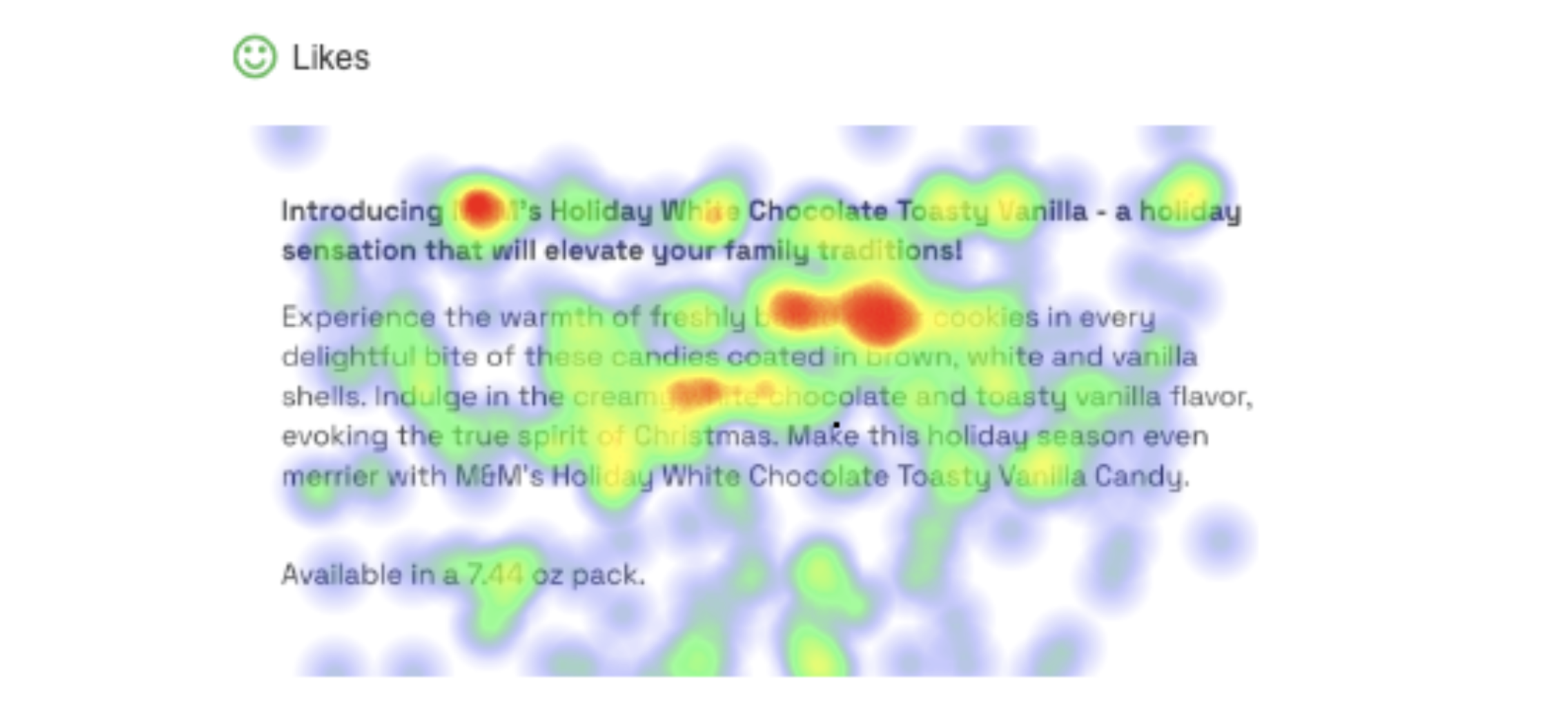

Finally, in our set of top performing products, there was a ‘new flavor’ product sitting within the “seed and grow” area of the classification grid: M&M’s White Chocolate Toasty Vanilla. The product scored significantly higher on Breakthrough Potential vs the average food product but didn’t showcase enough Trial Potential to sit within the top performing area of the grid. The product was seen as significantly distinctive (25.3% top box vs. 18.2% food norm) but purchase intent was very much in line with the norm (30.2% top box vs 29.5% food norm).

Generating trial is highly important for a seasonal product to generate return on investment. On the product description, M&M’s describes this new variant as tasting of sugar cookies — and people absolutely love that (as seen on the product description heat-map below). Sugar cookie was the second-most appealing Christmas flavor in our seasonal flavor analysis, so maybe M&M’s missed a trick when naming this seasonal product.

Products that didn’t make the nice list

Seven of the products we tested didn’t hit the mark on Trial Potential to generate the short-term sales desired for a seasonal product. But there’s a clear divide within these products — three of them showed a lot more promise than the rest.

Those three products — Lindor Holiday Peppermint Cookie Truffles, Oreo Marshmallow & Hot Cocoa Cookies and Haribo Candy Cane Gummies — performed in line with the average food product on Trial and Breakthrough Potential (between 48 and 61 percentiles). Purchase likelihood was on par with the norm (29.6% top box vs 29.5% food norm), they were relatively differentiated (21.9% top box vs 18.2% food norm) but not advantageous enough vs what already is on offer (18.6% top box vs 20.3% food norm).

Perceived taste may be the problem. All three products had very polarizing responses to their flavors — some absolutely loved them while others were on the fence. Perhaps some apprehension comes from the fact that all three brands are leaders in their category and have an iconic original product.

While hot cocoa ranked the most appealing flavor of the season and worked wonders for Hershey’s Kisses, consumers struggled to see how the flavor fit the Oreo brand. Peppermint ranked 14th on our list of flavors, but was also one of the most polarizing — it was ranked a top flavor and a bottom flavor almost an equal number of times.

The remaining four products sat within the lower third of all food products tested in terms of Trial Potential. Like the three products above, they also had divisive flavors, but the reasons for their low in-market potential differed:

Tony’s Gingerbread Milk Chocolate Bar: While we found gingerbread to be a polarizing flavor like peppermint, the biggest impact to trial potential was price. Consumers perceived it to be too expensive (69.9% bottom 2 box vs 46.7% food norm), and this had a major impact on purchase intent.

Trader Joe’s Mini Gingerbread People & Favorite Day Mini Sandwich Cookies: There was general appeal towards these products, just not enough against our food norm to drive higher levels of potential. Lacking differentiation and advantage, these products ultimately didn’t convince consumers to buy more frequently from the sweet baked snacks category, scoring significantly lower than average (44.4% top 2 box vs 52.6% food norm).

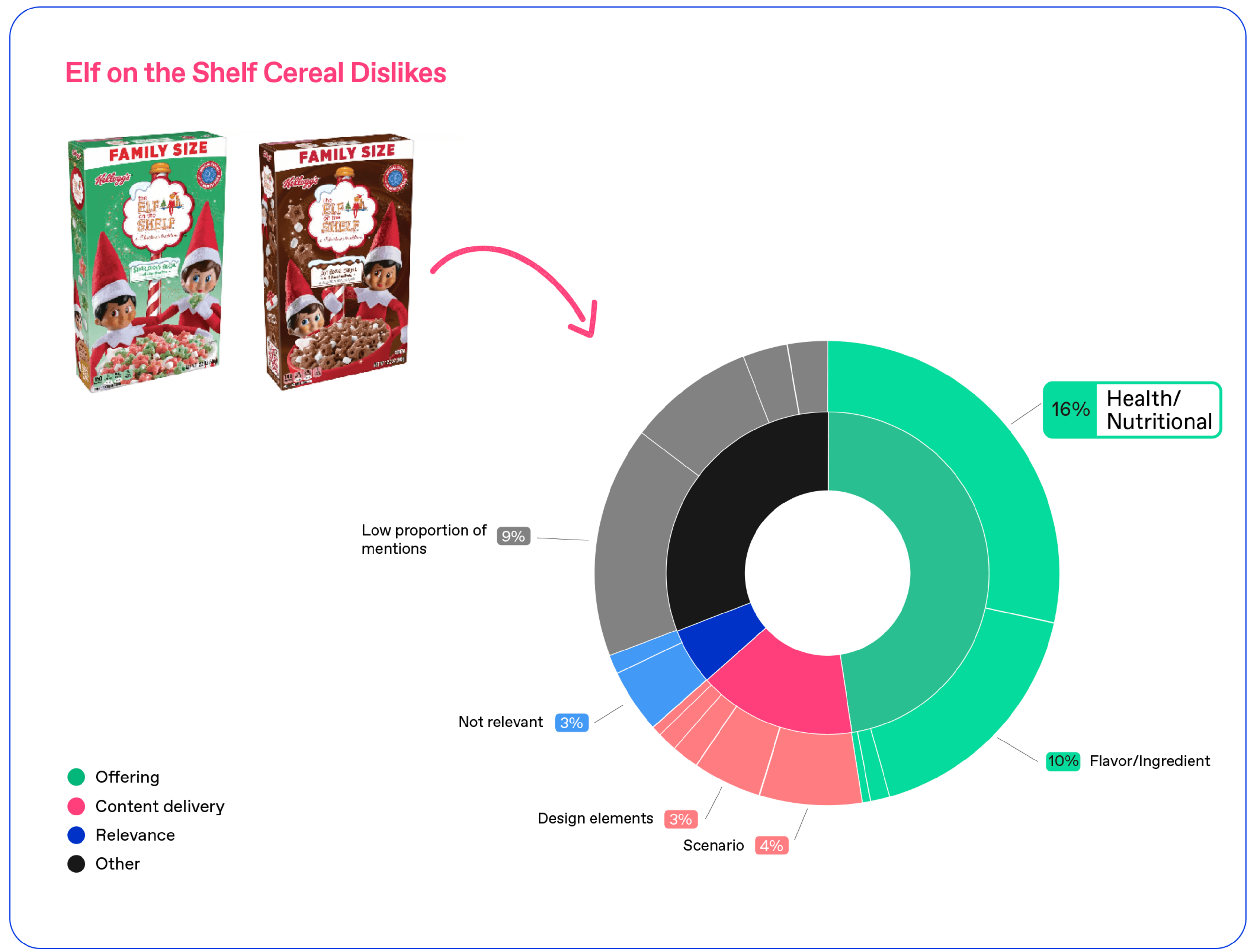

Kellogg’s Elf on the Shelf Cereal: Much like we saw on our halloween product analysis, consumers tend to be quite critical about the amount of sugar in cereal products. While consumers thought it was great for kids (54% agreement), they were concerned about the nutritional value of the product. One respondent said “It's just another sugar packed cereal aimed at kids that provides no nutritional value."

Looking at these 17 holiday products, there are clear consistencies with the trends we found in the performance of Halloween products, but a few differences too.

Elements to embrace:

We found similar success factors for the winter holidays as we did at Halloween:

Seasonally-relevant “minor” changes to core products — less is more! By maintaining the core product, particularly in taste, and making relevant changes to the packaging and product appearance, there is significantly less risk of losing out on appeal.

Seasonal cues that make sense for the brand and product. Packaging your product like a Santa hat, shaping it like a snowman or giving it Christmas colors works best if consumers see a connection or fit to the brand or original product.

But as opposed to what we saw at Halloween, for the holidays you can explore:

Consumer-informed seasonal flavors with the right brand fit. But when looking to embrace a new flavor for seasonal innovation, it’s important to first explore the appeal for it and understand whether it’s a good fit for your brand through consumer research.

Elements to watch out for:

Polarizing flavors. Peppermint and gingerbread are classic holiday flavors, but some love them and others hate them. Products with these flavors may not be as successful as more well-loved flavors like hot cocoa. Appealing to a narrow audience in the long-run can (on some occasions) generate a consistent and returning customer base; however, it can be limiting for seasonal products.

Category and brand relevance to the season. Some categories or brands have a greater connection to particular seasons. Playing in a category that has a strong presence during the season you are looking to innovate for is paramount in determining success.

Brand new products. These can be highly differentiated, generate excitement and work on some occasions. However, more often than not, they don't drive engagement from a wide enough range of consumers who inevitably compare them vs. original products available all year round.

There’s a lot we can learn from this year’s successful (and not so successful) innovations that can inform your holiday innovation next year.

The ultimate guide to successful seasonal innovation

Find out which elements make for a successful seasonal innovation and which you should watch out for based on consumer research.